After the Rush: APAC's mRNA and Vaccine Capacity Hangover

07 July 2026 | Tuesday | Analysis

In June 2022, South Korea had something it had wanted for two years: a COVID-19 vaccine of its own. SKYCovione, developed by SK bioscience with the University of Washington's Institute for Protein Design and backing from CEPI and the Gates Foundation, was a genuine scientific achievement — a locally made, refrigerator-stable shot that did not need the ultra-cold chain the mRNA leaders demanded. It was also, within a remarkably short window, a commercial casualty. By the time the plant was ready to run, the population had already been vaccinated with imported mRNA, the virus had drifted to variants the original design did not match, and demand for the domestic product collapsed. Production of the country's one home-grown COVID vaccine was halted not long after it launched.

SKYCovione is not, strictly, an mRNA story. But it is the cleanest available emblem of a condition now spreading quietly across Asia-Pacific's vaccine base: the hangover after the rush. Between 2020 and 2023, governments and companies across Thailand, India, Korea, Indonesia and beyond poured public money and corporate ambition into building — at genuine emergency speed — the capacity to make advanced vaccines, and mRNA in particular, on home soil. Much of that capacity now stands underused. The lines exist. The trained staff exist. What does not exist, in peacetime, is enough demand to fill them.

That gap between what was built and what is used sits at the centre of a debate that will shape the region's next decade of health security. On one side is the logic of preparedness, which holds that a warm production line is a form of insurance — expensive to keep, ruinous to lack when the next pathogen arrives. On the other is the logic of the balance sheet, which asks, reasonably, who is expected to pay to keep an idle asset ready, and for how long. Between pandemics, those two logics do not reconcile on their own.

▸ What got built, and what runs

The scale of the build-out is easy to underestimate now that the urgency has faded. Thailand offers the sharpest illustration. Chulalongkorn University's Chula Vaccine Research Center, led by immunologist Kiat Ruxrungtham, developed ChulaCov19 — Southeast Asia's first home-designed mRNA COVID vaccine — in collaboration with mRNA pioneer Drew Weissman at the University of Pennsylvania. The Thai government backed the effort with a grant reported at 2.3 billion baht, and manufacturing was handed to BioNet-Asia, a Franco-Thai vaccine maker whose plant north of Bangkok in Ayutthaya became one of only a handful of facilities anywhere capable of producing mRNA drug substance end to end. Ruxrungtham's stated ambition was explicit: to make Thailand an mRNA hub, capable of inventing, developing and producing vaccines fast enough to matter in the next crisis.

The science held up. The market did not arrive on schedule. Thailand had all but eliminated domestic transmission for long stretches, then vaccinated its population largely with imported product; a first-generation local COVID shot had little room left to fill. The programme pressed on with a second-generation bivalent candidate in clinical trials in Thailand and Australia, and BioNet has since broadened its base — winning EU good-manufacturing-practice certification in late 2025 and signing a regional partnership with Indonesia's state manufacturer Bio Farma on a combined pertussis-containing vaccine. But the core tension remains: a scarce, expensive-to-maintain mRNA capability, running well below what it was built to do.

India's arc rhymes. Pune-based Gennova Biopharmaceuticals, part of the Emcure group, developed the country's first mRNA vaccine, GEMCOVAC-19, with support from the Department of Biotechnology and BIRAC through the Mission COVID Suraksha programme, and followed it with an Omicron-specific booster, GEMCOVAC-OM, that won emergency authorisation in mid-2023. Both were thermostable and delivered needle-free, intradermally — engineered precisely for a country where ultra-cold logistics are a liability. Yet by the time the booster cleared, the domestic COVID emergency had passed and uptake was thin. The platform Gennova built to answer a pandemic found itself, like BioNet's, waiting for the next reason to run at scale.

The pattern extends beyond the three headline countries. Indonesia's state manufacturer Bio Farma, one of the developing world's largest vaccine producers by volume, took on mRNA fill-finish and technology-transfer commitments through the WHO programme, adding advanced capability to a base built for routine childhood immunisation. India's Serum Institute — the single largest vaccine maker on earth by doses — expanded aggressively during the pandemic and now carries surge capacity that only a genuine emergency could fully absorb. Across the region, the same shape recurs: an installed base sized, in a burst of 2020-21 conviction, for a once-in-a-century event, now metabolising a return to ordinary demand. The conviction was rational at the time. Waiting a year for imported vaccines, as much of Asia did in the first pandemic winter, was the alternative nobody wanted to repeat.

Korea's version is starker because the state spent so heavily on the wrong side of the ledger. Between 2020 and 2023, the government spent on the order of 7.6 trillion won importing vaccines while committing only a fraction of that — a few hundred billion won, spread thinly across dozens of separate projects — to building domestic capability, according to reporting in the Korean biomedical press. SKYCovione was the one product that reached market, and it did not last. SK bioscience has since pivoted hard toward a broader "vaccine ecosystem" — a new research and process-development centre in Songdo and expanded fill-finish capacity in Andong — and has signalled interest in adding mRNA, cell and gene therapy and viral-vector work to keep those assets busy. The company narrowed its losses in 2025 on the back of exports and contract manufacturing, which tells its own story about where the demand actually is: outside the domestic pandemic market that justified the build.

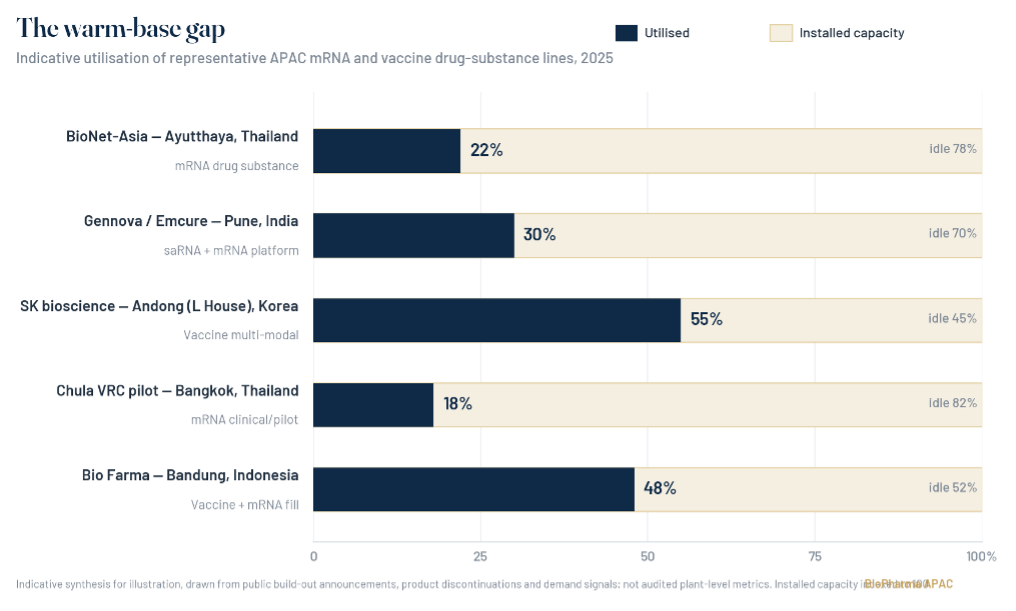

Read together, these are not failures of engineering. They are a structural mismatch. Emergency capital built capacity sized for a pandemic; peacetime demand is sized for routine immunisation and a handful of endemic threats. The indicative picture — drawn from public build-out announcements, product discontinuations and demand signals rather than audited plant metrics — is of advanced lines running at a fraction of nameplate capacity, with the newest and most specialised mRNA assets sitting idlest of all.

FIG. 1 The warm-base gap — indicative utilisation of representative APAC mRNA and vaccine drug-substance lines. Figures are an illustrative synthesis of public build-out announcements, product discontinuations and demand signals, not audited plant-level metrics.

▸ Four ways to look at one idle line

The same underused facility looks different depending on who is standing in front of it, and the region's decision will ultimately be a negotiation between four vantage points.

To a vaccine-manufacturing executive, an idle mRNA suite is a fixed cost that does not stop accruing when the orders do. Clean rooms must be maintained, cold storage powered, quality systems audited, and — most expensive of all — a specialised workforce retained, because the tacit knowledge of how to run an mRNA process cannot be furloughed and re-hired on demand. The executive's instinct, absent a paying customer, is to convert the asset to contract manufacturing for whoever will pay, or to repurpose it toward a commercial product, or, failing both, to quietly mothball it. None of those choices optimises for pandemic readiness; they optimise for survival.

To a pandemic-preparedness policy lead, that same line is a strategic reserve whose value cannot be read off this year's utilisation. The whole point of a reserve is that it looks wasteful right up until the moment it is indispensable. Their frustration is that the preparedness dividend is invisible and deferred while the maintenance cost is visible and immediate — a losing matchup in any budget negotiation. Their preferred instruments are the ones that convert readiness into a funded line item: warm-base retainers, standing volume guarantees, regional stockpile mandates.

To a health economist, the line is a problem of misaligned incentives and mispriced risk. The social value of warm capacity is enormous and diffuse; the private cost is concrete and borne by one firm; and markets systematically underprovide goods with that structure. The economist does not dispute that the capacity is worth keeping — the aggregate maths is overwhelming — but insists that wanting it is not the same as financing it, and that only a credible, multi-year commitment mechanism can bridge the two.

To an mRNA-platform scientist, the debate can look almost beside the point, because the technology's defining feature is its indifference to the target. The same suite that made a COVID vaccine can, with a new sequence, make a candidate against dengue, a personalised cancer therapy, or something not yet named — provided the platform stays live and the people who understand it stay in the building. For the scientist, the tragedy is not idle stainless steel; it is the dispersal of hard-won know-how if the line goes cold. Capacity, in their view, is ultimately measured in trained heads, not litres of bioreactor.

None of the four is wrong. The task is to build a settlement that satisfies enough of each at once.

▸ The case for keeping it warm

Against that ledger of underuse sits an argument that has only grown louder since 2020: that idle-but-ready capacity is the entire point, and that letting it decay would be a historic error.

The clearest articulation is the 100 Days Mission, launched under the UK's G7 presidency in 2021 through a partnership with CEPI and later embraced by the G20. Its target is deceptively simple — within roughly 100 days of identifying a pathogen with pandemic potential, the world should be able to develop, manufacture and begin deploying a safe, effective vaccine. During COVID-19, the first shots arrived in 326 days, and modellers at Imperial College London have estimated that compressing that to 100 days could have averted more than eight million deaths by the end of 2021. The mission's whole premise is that speed depends on standing infrastructure: platforms already validated, staff already trained, lines that can pivot rather than be poured from scratch. A vaccine in 100 days is impossible if the region has to rebuild its manufacturing base first.

That is where the warm-base logic and mRNA meet. The platform's defining virtue is that the same production process can, in principle, make a vaccine against almost anything by swapping the genetic sequence — the property that let Gennova's team describe its technology as disease-agnostic and pandemic-ready. A warm mRNA line in Bangkok or Pune is not just insurance for the disease it was built against; it is a general-purpose response asset for whatever comes next.

The World Health Organization's mRNA technology transfer programme has become the main institutional vehicle for spreading that capability across the global South. Launched in 2021 with the Medicines Patent Pool and a hub at Afrigen in Cape Town, the programme has enrolled 15 partners across Latin America, Africa, Eastern Europe and Asia — five of them in the Asia region, including Gennova in India, Bio Farma in Indonesia and partners in Bangladesh, Pakistan and Vietnam. In 2026 it moves into a second phase explicitly aimed at the harder problem: not proving the technology can be transferred, but making the resulting factories commercially sustainable. The programme's own literature is unusually candid about the crux. To keep facilities capable of pandemic response, they must be kept warm by producing mRNA products between pandemics; because the timing of the next one is unknown and appetite for indefinite subsidy is limited, those products need viable markets and steady revenue.

Southeast Asia has begun building exactly that — a pipeline of regionally relevant targets to keep the lines running. Under the WHO programme, research consortia have formed around diseases that matter locally: the International Vaccine Institute leading an mRNA dengue effort, Hilleman Labs working on hand, foot and mouth disease, and Chula VRC leading a therapeutic mRNA vaccine against human papillomavirus, a cancer-prevention play. The strategic logic is regional self-reliance, a phrase that recurs across the region's policy documents with new force after the "vaccine apartheid" of 2021, when high-income countries cornered early supply and the rest of the world waited. For governments that lived through that, a warm domestic line is not an accounting problem to be optimised away. It is sovereignty.

CEPI, for its part, is trying to institutionalise the warm-base idea at global scale. Its next strategic phase, framed as CEPI 3.0 and due to begin in 2027, is built around embedding rapid-response platforms directly with regional manufacturers and rehearsing the networks that would have to activate in an emergency — the organisational equivalent of keeping the engine turning over. The organisation's leadership has been unsparing about the stakes, arguing that recent outbreaks of Nipah, Ebola, Marburg and others are reminders that the next Disease X is a question of when, not whether, and that the tools to answer it in 100 days are, for the first time in history, within reach. What is not yet within reach is the sustained financing to keep those tools warm — a point the World Economic Forum's own tracking of regionalised vaccine manufacturing underlines, noting that three years of political commitments have yet to translate into the predictable demand, market access and financing that sustainable local production actually requires.

▸ Who pays for insurance nobody is claiming

And yet sovereignty does not, by itself, pay a facility's electricity bill. The economics of warm capacity are the hardest part of the whole equation, and they are where the preparedness argument tends to break down in practice.

Start with the size of the prize, because it is not small. Analysis summarised by the Center for Global Development suggests that investing roughly 60 billion dollars up front and around 5 billion dollars a year thereafter in advance manufacturing capacity — enough to vaccinate 70 percent of the world against a new virus within six months — could generate well over 500 billion dollars in social value. On those numbers, pandemic capacity is a textbook global public good: hugely valuable in aggregate, and chronically underfunded because no single buyer captures the return. A US National Academies analysis made the same point more bluntly, noting that paying for overcapacity to deliver vaccines in a pandemic is, viewed globally, an inexpensive and highly rational strategy.

The trouble is that "viewed globally" is not how budgets are set. A public good that benefits everyone tends to be paid for by no one, and the private manufacturer left holding an idle line does not get to bill the world for the insurance it is providing. The COVID demand spike proved the point in reverse: when it collapsed, it was the smaller tier-two and tier-three suppliers who hit financial distress, having tooled up for a surge that evaporated. Manufacturers cannot sustain production, as one strand of the diversification research puts it plainly, without strong and predictable demand — and predictable demand is exactly what peacetime does not supply.

That leaves a familiar menu of financing models, none of them complete. Advance purchase commitments and volume guarantees — governments or pooled buyers promising to buy a minimum, whether or not a pandemic comes — can de-risk the fixed investment enough to justify keeping a line warm; the difficulty is that most APAC national markets are individually too small to anchor a GMP-grade mRNA facility, which is why the WHO's second phase leans so heavily on pooled procurement and cross-border alignment. Standing "warm-base" retainers, in which a state effectively pays a manufacturer a fee to hold capacity in readiness the way an air force pays to keep jets fuelled, are cleaner in theory but politically fragile, competing every budget cycle with schools and hospitals that produce visible results now. And the international money that might have bridged the gap is thinning: development assistance for health is plateauing or declining, donor priorities are shifting, and CEPI's own preparedness scorecard has recorded a sharp fall in research-and-development funding since 2022, with therapeutics funding dropping by more than half in a single year and the entire enterprise dangerously dependent on a single dominant funder, the US government.

The uncomfortable synthesis is that the preparedness case is strongest at exactly the altitude — global, multi-year, probabilistic — at which no one has to write the cheque, and weakest at the altitude where someone does. Warm capacity is insurance almost everyone agrees is worth holding and almost no one wants to be the one to buy.

Warm capacity is insurance almost everyone agrees is worth holding — and almost no one wants to be the one to buy.

▸ The bridge: mRNA beyond COVID

If subsidy is fragile and pooled procurement is slow, there is a third path that many in the region are betting on: give the lines something commercial to make. The most promising bridge is the platform's own expansion beyond COVID — into oncology, rare disease and endemic infections — turning pandemic insurance into a business that can partly pay for itself.

The oncology case is the one investors watch. Moderna's individualised neoantigen therapy, intismeran autogene, developed with Merck, has moved into a broad Phase 3 programme spanning melanoma, non-small-cell lung, bladder and renal cancers, after mid-stage melanoma data showed a meaningful reduction in the risk of recurrence when the personalised mRNA vaccine was added to Merck's checkpoint inhibitor. BioNTech is advancing its own cancer candidates; the wider field has shifted, in the space of a few years, from pandemic tool to personalised-medicine platform. For a warm mRNA line, personalised cancer vaccines are an almost ideal peacetime tenant: they demand exactly the flexible, small-batch, sequence-swapping capability the technology was built around, and — unlike a pandemic — they generate steady, year-round demand.

Rare disease points the same way. Moderna's mRNA therapeutics for propionic acidemia and methylmalonic acidemia have reached registrational-stage studies, extending the platform from prevention into treatment. These are not APAC programmes today, and personalised or ultra-rare products are not simple to localise. But they establish the principle that matters for the region's stranded lines: mRNA is a manufacturing platform, not a single product, and a facility validated for one output can, with investment, be pointed at others.

Closer to home, the endemic pipeline is the more realistic near-term filler. The WHO consortia targeting dengue, hand-foot-and-mouth disease and HPV are, read commercially, a strategy to keep Southeast Asian lines busy with products the region actually needs year-round rather than only in a crisis. Seasonal influenza, RSV and HPV are the volume markets that could anchor utilisation; Moderna's own effort to expand its respiratory franchise shows where the steady demand is expected to sit. And the pandemic-preparedness mission itself is generating work: Gennova's collaboration with CEPI on a self-amplifying mRNA vaccine against Nipah virus — a paramyxovirus with a case-fatality rate that can approach three-quarters, and recurrent outbreaks in India — expanded in 2025 to funding worth up to 13.4 million dollars, pairing the company's saRNA platform with AI-designed antigens. Nipah will never be a blockbuster. But CEPI-backed work of exactly this kind is one of the few mechanisms that pays a warm line to stay warm while pointing it at a real regional threat.

None of this fully closes the gap. Oncology and rare-disease manufacturing are technically demanding and geographically concentrated; the endemic vaccines that could fill APAC lines are lower-margin and slow to license; and a facility optimised for personalised cancer therapy is not instantly a pandemic-response asset. Repurposing buys time and defrays cost. It does not, on its own, guarantee that the specific capability the region wants for the next Disease X will still be humming when it is needed.

▸ The decision the region is making by not deciding

Five years on from the emergency that built it, APAC's advanced vaccine base sits at a quiet crossroads. The capacity is real and, in places, world-class. The preparedness argument for keeping it warm is, at the global level, close to unanswerable. The financing to do so is unresolved, the international money is thinning, and the demand that would keep the lines running commercially is arriving unevenly and mostly from outside the pandemic use-case that justified the investment.

The likeliest outcome is not a dramatic decision either way, but drift — the slow, unglamorous decay of lines that are neither funded as insurance nor filled by the market, staff who move on, certifications that lapse, tacit know-how that quietly disperses. That is how hard-won capacity is usually lost: not in a cancellation announcement, but in a budget that is simply not renewed. Whether the region treats its pandemic base as an asset worth a deliberate, funded decision — through pooled procurement, warm-base retainers, an expanded repurposing pipeline, or some combination — or lets it quietly wind down and hopes the next emergency gives enough warning to rebuild, is the choice now being made across Asia-Pacific. It is being made, for the most part, by default.

The rush built the capacity. The hangover will decide whether the region gets to keep it.

arcilla.fran@biopharmaapac.com

|

DISCLAIMER This feature is an editorial analysis prepared by BioPharma APAC for information and discussion purposes only. It synthesises publicly available information — including company announcements, government and multilateral statements, peer-reviewed and policy literature, and press reporting — current as of publication; details may have changed since. Statements attributed to named individuals or organisations are drawn from public sources and are paraphrased for length; they are not original interviews conducted for this article unless expressly stated. The capacity-utilisation chart is an indicative synthesis for illustration, based on public build-out announcements, product discontinuations and demand signals, and does not represent audited plant-level metrics or any individual company's disclosed utilisation figures. Nothing here constitutes investment, regulatory, legal or medical advice, or a recommendation regarding any company, security or product. Readers should independently verify facts before relying on them. Views expressed are those of the editorial desk and do not necessarily reflect those of any organisation mentioned. © BioPharma APAC. All rights reserved. |

Most Read

- How Does GLP-1 Work?

- Innovations In Magnetic Resonance Imaging Introduced By United Imaging

- Management of Relapsed/Refractory Multiple Myeloma

- 2025 Drug Approvals, Decoded: What Every Biopharma Leader Needs to Know

- BioPharma Manufacturing Resilience: Lessons From Capacity Expansion and Supply Chain Resets from 2025

- APAC Biopharma Review 2025: Innovation, Investment, and Influence on the Global Stage

- Top 25 Biotech Innovations Redefining Health And Planet In 2025

- The New AI Gold Rush: Western Pharma’s Billion-Dollar Bet on Chinese Biotech

- Single-Use Systems Are Rewiring Biopharma Manufacturing

- The State of Biotech and Life Science Jobs in Asia Pacific – 2025

- Asia-Pacific Leads the Charge: Latest Global BioSupplier Technologies of 2025

- Invisible Threats, Visible Risks: How the Nitrosamine Crisis Reshaped Asia’s Pharmaceutical Quality Landscape

Bio Jobs

- Sanofi Turns The Page As Belén Garijo Steps In And Paul Hudson Steps Out

- Global Survey Reveals Nearly 40% of Employees Facing Fertility Challenges Consider Leaving Their Jobs

- BioMed X and AbbVie Begin Global Search for Bold Neuroscience Talent To Decode the Biology of Anhedonia

- Thermo Fisher Expands Bengaluru R&D Centre to Advance Antibody Innovation and Strengthen India’s Life Sciences Ecosystem

- Accord Plasma (Intas Group) Acquires Prothya Biosolutions to Expand Global Plasma Capabilities

- ACG Announces $200 Million Investment to Establish First U.S. Capsule Manufacturing Facility in Atlanta

- AstraZeneca Invests $4.5 Billion to Build Advanced Manufacturing Facility in Virginia, Expanding U.S. Medicine Production

News

Editor Picks